From a Recovering CPA Who Still Loves a Good Spreadsheet

“Half the money I spend on advertising is wasted; the trouble is, I don’t know which half.” The line is most often credited to retailer John Wanamaker, though the exact origin is debated and sometimes tied to Lord Leverhulme. The point stands—and it still stings.

A little context about me: I was a CPA many years ago. I’m no longer licensed—much to the disappointment of my mother, Annetta. But she thinks I’m brilliant and loves me just the same.

Still, that training means I lean on numbers and mechanics when I assess problems, especially marketing. Marketing can look amorphous or “huggy-feely.” But with a fair set of rules, we can tell—in the aggregate—whether the work is bearing fruit, where to move the next dollar, and when to stop spending.

Below is the simple, owner-friendly system I use. It works for short sales cycles. With one twist, it also works when your deals take 6–24 months (custom manufacturing, engineered-to-order, B2B services).

Step 1: Run Marketing With Three Ledgers

My finance brain likes ledgers, so I use three:

1. Ad Platforms (Acquisition Ledger):

What every channel claims: Google, Meta, LinkedIn, industry directories, trade shows, referrals.

2. CRM (Pipeline Ledger):

What Sales is working: Leads, quotes/opportunities, source fields, stages, close dates, deal amounts.

3. Accounting (Cash Ledger):

What the bank confirms: Invoices, collections, refunds, COGS, margin.

Rule of thumb: when the ledgers disagree, Cash wins, CRM reconciles to Cash, and ad platforms get credit—not blind trust. That’s not anti-marketing. It’s pro-decision.

Step 2: Add a “Ground-Truth Ladder” for Long Sales Cycles

If your close time is 6–24 months, “cash wins” is too slow to steer day-to-day. So we move one rung up for attribution while keeping cash as financial reality:

- Cash (Collections): Finance truth for GAAP, margin, solvency.

- AR / Revenue Recognition: Invoiced and recognized revenue (milestones, % of completion).

- Bookings / Orders (POs/SOWs/LOIs): The commercial truth for marketing and sales. This is the win we attribute to channels.

- Qualified Opportunities / Quotes: The leading truth: early signal on quality and velocity.

Policy: Optimize marketing to Bookings. Run the company to Cash. Reconcile all four truths so no one is flying blind.

Step 3: Stop Double-Counting With a Simple Truth Table

You get one—and only one—Primary Source per contact/deal. Pick a priority stack and live by it:

- If utm_campaign or campaign_id matches a known paid campaign → Paid (map to Paid Search, Paid Social, etc.)

- If the referrer domain is your email platform’s tracking domain → Email

- If the referrer contains linkedin.com, facebook.com, instagram.com, or t.co and there’s no paid flag → Organic Social

- If the referrer contains a partner’s domain or a tracked referral link → Partner/Referral

- If the landing path starts with /tradeshows/ or the form says “Event = X” → Event/Trade Show

- If the referrer contains google./bing. and there’s no paid flag → Organic Search

- If there’s no referrer and no campaign data → Direct/Type-In

Two guardrails keep this honest:

1. A Manual Override field for Sales Ops (rare, reason required)

2. An Influenced By multi-select for assists (webinar, retargeting, white paper)… These never replace Primary Source

Add a one-page Data Dictionary so “Lead,” “SQL,” “Win,” “Primary Source,” “Gross Margin,” etc., mean the same thing to everyone.

A Quick Note on “Full Journey” Attribution

Look, I know this feels overly simple. Every touchpoint does build value—that PPC click that introduced them, the white paper download, the webinar attendance, the retargeting ads they saw for weeks. In reality, it’s the full investment working together that closes deals.

In my first Cost Accounting class at the University of Akron, my professor warned us: “The more complex your allocation models get, the more wrong your decisions become.” He was talking about overhead allocation, but it applies perfectly to marketing attribution.

You could build a system that splits credit across every touchpoint, weights them by position and timing, and calculates blended CACs across the full journey. Some companies do this. But I’ve found that operational clarity beats mathematical precision every time. The Primary Source truth table gives you clean budget decisions. Complex multi-touch attribution gives you beautiful dashboards and paralyzed decision-making.

Keep it simple. If you want to track the broader investment story, do it as a separate analysis—total marketing spend divided by total new bookings—not as your day-to-day attribution engine.

Step 4: A One-Hour Monthly Close (Lock by the 10th)

Close the prior month on the 10th to give Finance time to post late invoices. Invite CEO, Finance, Sales/RevOps, and Marketing. The agenda:

- Reality Check (Cash & AR): Collections vs plan, cash position, WIP, gross margin.

- Bookings Performance (Marketing/Sales truth): New booked customers and dollars by Primary Source.

- Cohort Health (Leading Indicators): Quotes issued, win rates, pipeline aging, velocity by source. Is each cohort tracking its historical win curve?

- Attribution Discipline: Apply the Truth Table, freeze Primary Source on wins, and log any overrides in an Exceptions Log.

- Decisions: Shift budget by source based on cohort trajectory and payback to bookings, not short-term cash noise.

Freeze policy: once a month is locked, don’t rewrite history. True-ups flow into the current month with dated notes.

Step 5: The Only Four Numbers I (Still) Care About

I love dashboards. I really only need four numbers to steer:

1. Customer Acquisition Cost (CAC):

Formula: CAC = (All acquisition costs in period) ÷ (New customers booked in that period) Acquisition costs = media + agency + content tied to acquisition + attributable tools.

2. Payback Period (run two versions):

Payback to Bookings (expected): first month where expected gross margin from booked deals ≥ CAC, using your standard recognition curve (example: 20% deposit, 50% at start, 30% at delivery). • Payback to Cash (realized): first month where recognized gross margin (actual invoices/collections) ≥ CAC.

3. LTV:

CAC Formula: LTV = Avg. Gross Margin per period × Expected Retention (periods) Use booked LTV for forward planning and realized LTV for backward validation. Target >3:1; >4:1 gives you room to invest.

4. Marketing-Sourced Contribution:

Formula: Gross Profit from marketing-sourced wins – Acquisition costs This keeps “volume” honest. Profit beats vanity.

Step 6: Cohorts and Win Curves (Your Long-Cycle Superpower)

Don’t judge a channel by same-month cash if your jobs land months later. Judge by cohorts:

- Create monthly Lead Cohorts by Primary Source (anchor on first qualified opp/RFQ—pick one rule and stick to it).

- Track each cohort’s Win Curve: % that convert to Bookings by 3, 6, 12, 18, 24 months.

- Run quarterly true-ups: when older opportunities book, credit those bookings back to their originating cohort month.

- Use a 24-month attribution window (or whatever matches your longest cycle).

This is how you avoid cutting a channel at month two when history shows it peaks at months 8–14.

A Concrete Example (Custom Metal Fabricator)

- January cohort (Organic Search): 60 qualified RFQs

- Historical Win Curve for Organic Search: 10% booked by month 6, 22% by month 12, 26% by month 18

- By September (M+8) you’ve booked 11 jobs (≈18%). You’re on curve.

Unit economics:

- January Organic Search spend (media + content + tool share): $18,000

- CAC (by bookings): $18,000 ÷ 11 = $1,636

- Expected gross margin per booked job: $25,000 (based on mix)

- Booked LTV:CAC (forward): If LTV per job is $25,000 and a typical customer does 1.3 projects, booked LTV ≈ $32,500 → LTV:CAC ≈ 19.9:1

- With a recognition curve (20/50/30), Payback to Bookings may land ~5–6 months after the median booking month; Payback to Cash trails by another 6–10 months depending on terms and collections.

Decision: Keep funding Organic Search because bookings are pacing to plan, even though cash lags. If LinkedIn’s January cohort is off-curve at M+8 (say 5% booked vs. historical 15%), throttle spend now—don’t wait a year for cash to confirm what the curve already told you.

What to Watch Weekly (So You’re Not Flying Blind)

While you wait for bookings or cash, monitor:

- Qualified RFQs/Opps per Source (are we getting real shots on goal?)

- Quote-to-Win Rate by Source (quality)

- Cycle Time by Source (days to quote; days to booking)

- Average Booked GM per Win by Source (are we attracting bigger, better-margin work?)

- Follow-Up SLAs (speed to first touch and to quote)

- Pipeline Hygiene (stale opps > X days at stage)

These leading indicators let you cut bad spend before the bookings arrive.

30/60/90: How I’d Roll This Out

Days 0–30: Foundations

- Publish your Data Dictionary and Truth Table

- Add CRM fields: Primary Source (single-select, required), Influenced By (multi-select), Original Cohort Month

- Enforce UTM discipline with a one-page builder for any budget request

- Choose your cohort anchor (first qualified opp/RFQ) and your recognition template (e.g., 20/50/30)

Days 31–60: Cadence & Visibility

- Launch the M+10 monthly close with the five-part agenda above

- Stand up two dashboards: Bookings Payback and Cash Payback (same CAC, different denominators)

- Start the Exceptions Log and Freeze Policy

Days 61–90: Backfill & Budget Rules

- Backfill the last three months with Primary Source and cohort month; apply the Truth Table retroactively

- Set budget re-allocation rules:

- Sources with off-curve cohorts at M+6 get a 25% cut

- Sources with <6-month payback to bookings get +15% (within your overall “salary-cap” for marketing)

- Document changes like journal entries so next month’s story has context.

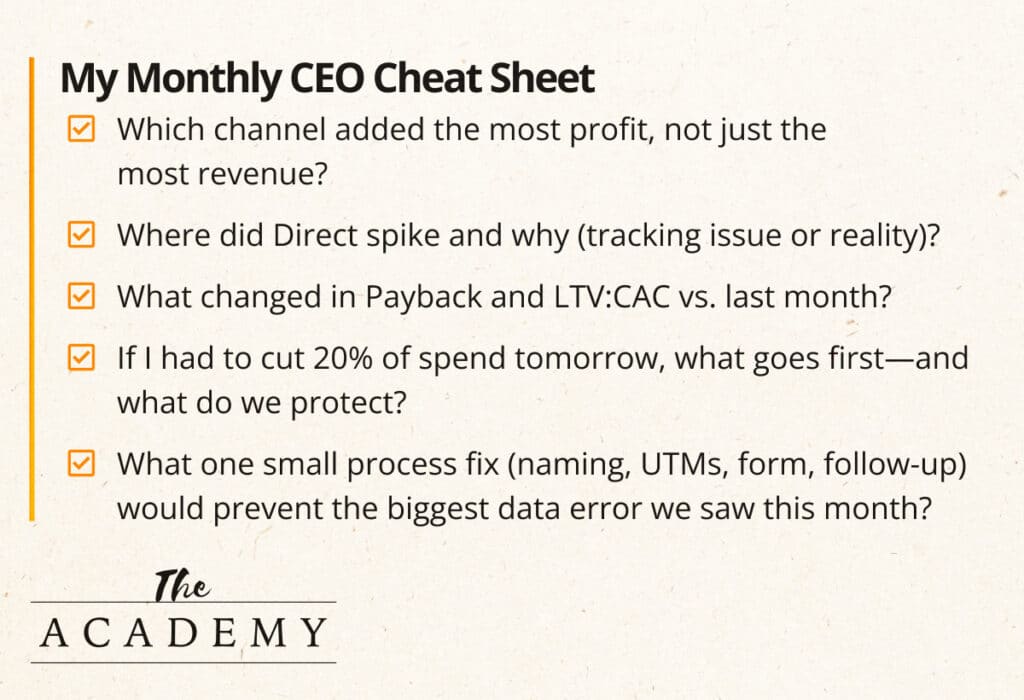

My Monthly CEO Cheat Sheet

I ask my team five questions, out loud, every month:

- Which channel added the most profit, not just the most revenue?

- Where did Direct spike and why (tracking issue or reality)?

- What changed in Payback and LTV:CAC vs. last month?

- If I had to cut 20% of spend tomorrow, what goes first—and what do we protect?

- What one small process fix (naming, UTMs, form, follow-up) would prevent the biggest data error we saw this month?

Final Thought

Look, I realize not everyone loves a spreadsheet like I do. Accounting is one thing, marketing is another. But marketing doesn’t work without accountability and measurable ROI. The creative side needs the numbers side—they’re not enemies, they’re partners.

Perfect attribution isn’t the goal. Consistent rules, a calm monthly close, and four honest numbers will get you most of the way there. For long cycles, tie attribution to Bookings and run the company on Cash.

Related Articles:

Why Your Website Is the Center of Your Inbound Marketing…

Many companies invest in digital marketing tactics like social media, email campaigns, and paid advertising. But without a strong website at the center of those…

What Your Marketing Report Should Actually Tell You

When you invest in digital marketing, you expect to see results. Reporting is one of the primary ways those results are communicated. Each month, a…

The Importance of Clear Calls to Action in Content Marketing

Content marketing is often celebrated for its ability to educate, build trust, and attract potential customers. Organizations invest significant time creating blogs, guides, videos, and…

Most Popular Articles

Seeing Favicons in Your Google Search Results? Here’s Why…

Have you noticed anything different in your Google Search results lately? Google added tiny favicon icons to its organic search results in January. It was…

AI or Agency? The pros and cons of a human touch vs artificial intelligence in web design

Your organization’s website is a critical marketing channel. It’s the first impression many customers have of your business and it plays a vital role in…

Business Growth and Digital Marketing News & Tips 11-17-24

Are you encouraging and rewarding innovation? Lee Cockerell is the former Executive Vice President of Operations at Walt Disney World. A lover of traditional red…