It should be a business’ goal to extract as much value out of each customer as possible. It’s hard to acquire customers, so you want to do what you can to keep them around over the long run.

A good metric to monitor on this topic is customer lifetime value. When you understand how much a customer is worth to your business, you can make some smart decisions about marketing tactics, sales follow-ups, and much more. Whether this isn’t something you’ve thought about previously in your business, or you just need a refresher, the article below should be a helpful resource.

What is Customer Lifetime Value?

This is a case where the name pretty much says it all. The metric of customer lifetime value is one that tracks exactly how much a customer is worth to your business in total. Rather than just counting their first purchase, or the purchases they make in the first year, customer lifetime value determines how much each customer is worth, on average, from start to finish.

It’s common for smaller businesses not to have a strong grasp of this number and what it means for how they operate. So if you aren’t familiar with this metric, don’t worry! But when you think about it a little closer, it makes sense that it’s important to know. If you don’t know how much a customer is worth to you, how could you possibly know how much you should be willing to spend to acquire that customer? We’ll have more on that later in the article, as well.

How to Calculate CLV

Don’t be scared off by the prospect of needing to do a little math in this section. The math itself is really quite simple – the only challenging part may come in tracking down the numbers you need to do your calculations. Once you have those numbers in place, and you can trust them as being accurate and reliable, it will just be a matter of turning to your calculator to uncover the answers.

Before we explain how to do this math properly, we want to stop quickly and explain how not to do this math. You might be tempted to simply track some of your customers over time to see how much they wind up spending with you. By sampling a small percentage of your customer base, it might seem like you could get a good idea of their lifetime value. But that’s not going to give you an accurate representation, as selection bias and other issues could come into play.

Instead, you are going to utilize averages across your customer base to then arrive at a number that is representative of your customer lifetime value across the board. This will be what you can expect the average customer to spend, and you can then use that number for a variety of purposes later on.

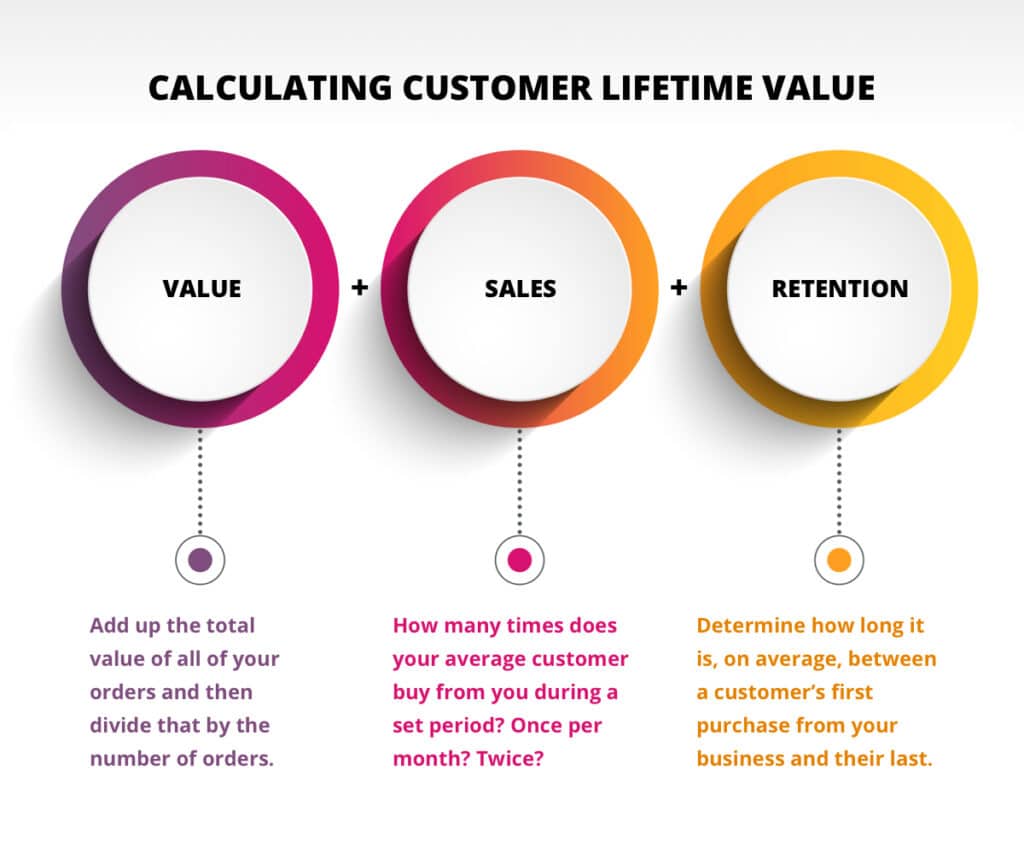

To do our math, we are going to require three numbers that you should be able to extract from the system you use to track sales and revenue.

- Average order value. This is a great starting point because it should be pretty easy to nail down. When you add up the total value of all of your orders for a given time period, and then divide that by the number of orders, what you are left with is the average value of each order that is placed. You’ll want to find this number and save it for use in our equation below.

- Transactions per period. How many times does your average customer buy from you during a set period? You’ll want to adjust this period to make sense for your business, but let’s say that you are going to use one month as your timeframe. Does a typical customer buy from you once each month? Twice? Or maybe they buy a couple of times per year, leaving you with a fractional sale each month? Whatever the case, this is the second number you will need to know.

- Customer retention. Lastly, you want to determine how long it is, on average, between a customer’s first purchase from your business and their last. You can use historical sales records to figure this out, and you’ll want to establish a cut-off to help you decide which customers in your database are done buying from you. For example, you might decide that anyone who hasn’t purchased in the last year can be ruled out for future purchases and therefore included in this calculation. Remember to keep the time frame the same between your transactions per period number and your customer retention number. So, if you used months in one category, use months again in the other.

To summarize, the three numbers you will want to have in hand are: 1.) your average order value, 2.) the number of transactions an average customer completes in a set time period, and 3.) how long the average customer stays with you. From there, you’ll need to do nothing more than multiply those three numbers together to come away with your customer lifetime value metric.

A Quick Example

Let’s walk through an example of the math just to make sure everything is clear. We’ll keep the numbers easy for the sake of discussion, but they’ll obviously look much different in the real world.

Imagine that the average value of each order that comes into your business is $10. Since your products are so affordable, each customer makes an average of three purchases per month, and the average customer sticks with your brand for two years, or 24 months. With that information, we have everything we need to do our calculation.

Multiplying the $10 order value by the rate of three purchases per month and 24 months’ worth of purchases leaves us with a customer lifetime value of $720. That means that the average new customer you bring into your company is going to spend $720 before they move on. Is that good? Well, there really isn’t a “good” or “bad” on this metric, as it’s all relative. For some businesses, that could be a great number – and for others, it could be a disaster. Below we’ll talk about how you can use the number you’ve calculated to see how things are going and what you can improve.

The Importance of This Metric

As an obvious starting point, the best reason to know your customer lifetime value is that it will inform you on how much you can afford to spend on marketing in order to acquire a new customer. If you are spending more per conversion than the customer is going to spend with you in total, something is obviously very wrong.

With our example above, a customer lifetime value of $720 could be very nice if the business only spent $100 to acquire that customer. But what if you had to spend $1,000 to get the same customer? That wouldn’t be a sustainable path, and you’d need to make some dramatic changes if you wanted to continue with the business.

So, in the big picture, you can use customer lifetime value to evaluate your marketing efforts and how they compare to the revenues they generate. But the usefulness of this metric goes far beyond that overview. Many businesses will segment their customers and calculate average lifetime values for each of those segments, leading to even more useful data.

For instance, you might have two distinct product lines that you sell – one that is upscale and has a higher price point, and one that is more budget-friendly. Breaking out your customers into those two groups and calculating the lifetime value for each will reveal which side of the business is truly more productive. That way, you’ll know which category you can spend more marketing money on, and you might even find that one product line isn’t worth continuing anymore.

Taking Steps to Improve

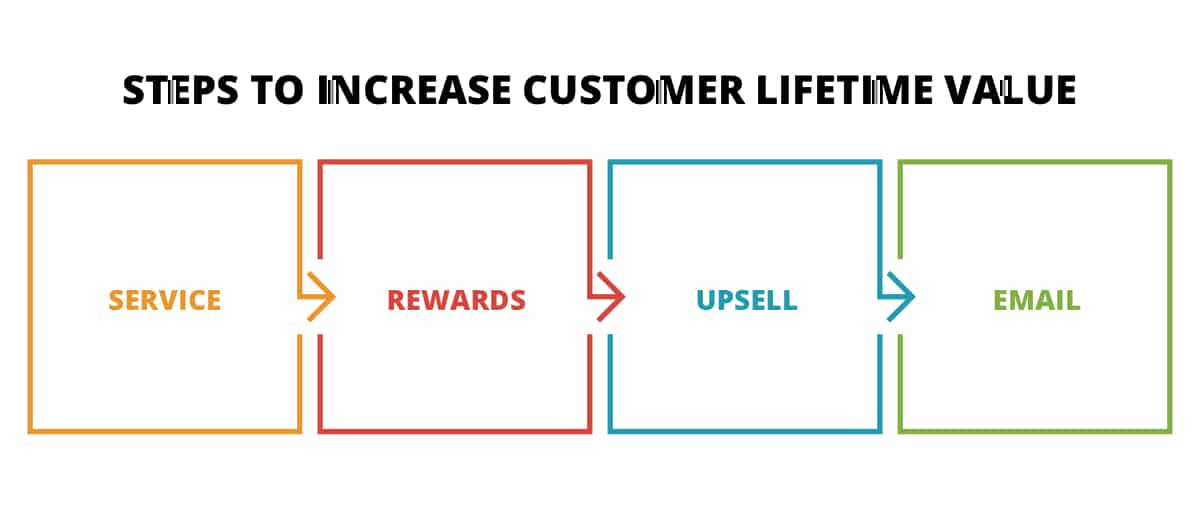

Once you know the customer lifetime value for your business, or for segments of your business, the next question is obvious – how do we drive this number higher? Getting more value from the customers you attract is one of the best ways to rise above the competition. Here are a few tips that you may want to consider carefully on this topic.

- Upgrade your customer service. Offering great customer service is one of the leading ways to add to lifetime value. The reasoning is simple enough – if people have a good experience with your brand, they are far more likely to come back. This is particularly true if they have an issue with a product or service and they are quickly refunded or provided some other type of support. When you show that you care about the customer and their satisfaction, that customer will wind up caring about your business in return.

- Build a rewards program. This is another way to build brand loyalty, and it has been made easier thanks to our modern, high-tech world. If you implement a rewards program using any of a number of different available platforms and systems, you can encourage people to stick with your brand rather than straying to the competition over time.

- Master the art of the upsell. Raising your average sale value is going to directly impact customer lifetime value, so work on upsell strategies that can make your ticket prices higher each time a purchase is completed.

- Use email marketing. It’s particularly important for businesses with a low purchase frequency to keep in touch with their existing customer base. Since people aren’t buying from you often, you want to stay relevant in their minds by checking in from time to time. Something like a monthly newsletter that goes out to subscribers can go a long way toward keeping the customer list engaged and ready to buy from you when the need arises.

Knowing the average value that each new customer brings to your business allows you to make solid decisions based on hard data. You don’t have to guess if your marketing costs are worthwhile, because you can compare how much it costs to get a customer to how much that customer will be worth in the long run. Get to work right away on calculating this number and keep it up-to-date as the performance of your business changes over time.

Related Articles:

Stop Posting. Start Connecting: The Case for Integrated Social Marketing

A brand with 50,000 followers and flat sales isn't a social media problem. It's a strategy problem. Many companies still think, "If we just grow…

Why Persona-Based Content Is Critical for AI Search Rankings

When we talk about personas, we're not talking about who you channel in the mirror when you get dressed in the morning. We're talking about…

The Long Game: Why B2B Content Marketing Pays Off When…

A few months ago, I picked up bread baking. Not as a grand ambition, but as a desire to do more with my hands and…

Most Popular Articles

Seeing Favicons in Your Google Search Results? Here’s Why…

Have you noticed anything different in your Google Search results lately? Google added tiny favicon icons to its organic search results in January. It was…

How to Use Email Analytics and Metrics to Measure Success

Email marketing remains one of the most effective digital marketing strategies, but success doesn't come from simply sending messages out into the abyss. To truly…

AI or Agency? The pros and cons of a human touch vs artificial intelligence in web design

Your organization’s website is a critical marketing channel. It’s the first impression many customers have of your business and it plays a vital role in…